Write off Bad Debts

Updated Mar 24th, 2026

Who is this guide for?

Accounts Users and Accounts Supervisors

This guide will show you how to write off any bad debts

If you sell an item or provide a service to a customer but the customer never pays you, you can reclaim the VAT you charged and paid to HMRC. HMRC calls this ‘bad debt relief’.

If you sell vatable goods or services to a customer, you will normally have paid the VAT element – the output tax – to HMRC. If the customer doesn’t pay you, you can claim bad debt relief and get back the VAT that you paid.

You can reclaim VAT that you paid to HMRC and which you have not received from the customer. The conditions are that:

● this debt is more than six months old, and less than three years six months old

● you have written off the debt in your VAT accounts and transferred it to a separate bad debt account

● debt has not been sold or handed to a factoring company

● you did not charge more than the normal selling price for the items

If you are entitled to claim bad debt relief, you add the amount of VAT you are reclaiming to the amount of VAT you are reclaiming on your purchases (input tax) and put the total figure in Box 4 of your VAT return.

To work out how much bad debt relief you can claim on a VAT inclusive balance, you need to apply the VAT fraction to the unpaid amount. For standard-rated supplies this is 7/47.

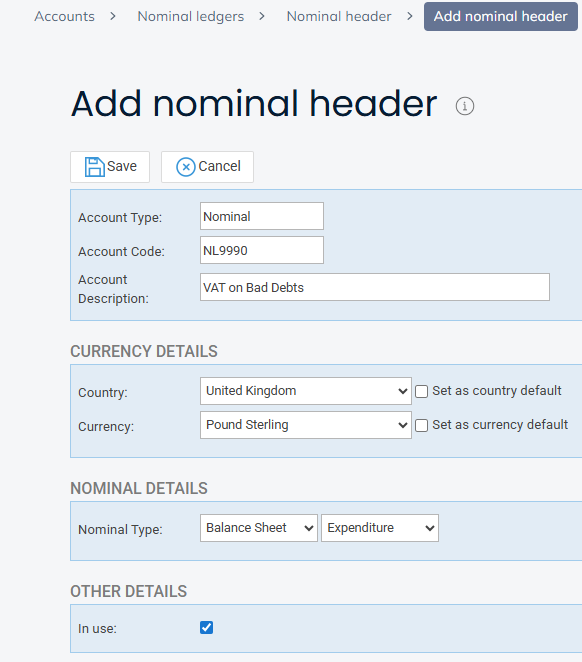

As the client’s ledgers only record outputs for VAT purposes, it is necessary to move the VAT element to a Balance Sheet nominal account.

If a nominal does not already exist for this purpose, you will need to open one. The Nominal will be a balance sheet Expenditure and should not be excluded from VAT.

- Nominal Type – Balance Sheet

- VAT Type – Expenditure

- Exclude from VAT – No

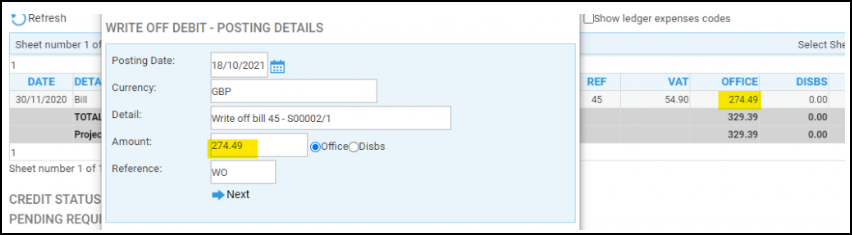

Write off the costs balance from the client ledger

From the client’s ledger card select the posting type write off debit and post. Here we write off the costs element only. It is useful to put the customer’s account number as part of the posting text for ease of reference. Ensure you select the correct radio button depending on the debt being office or disbursements.

Click Next, then ensure you allocate the write off posting against the bill or entry you are writing off.

Click Post. The costs are now written off.

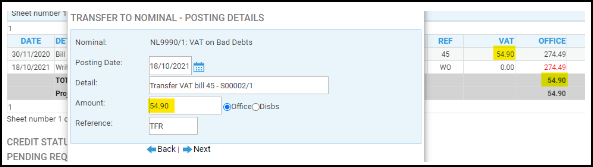

Transfer the amount of VAT from the client ledger to your Bad Debt nominal

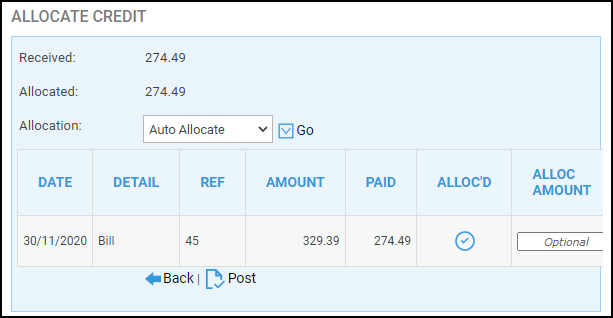

Next, select the posting type ‘n – Transfer to nominal’, and select ‘Post’. Complete the date and posting details and amount to write off the VAT element. Change the radio button to Office, not Disbs.

Enter the Nominal account, remembering to add the /1 for the SAC.

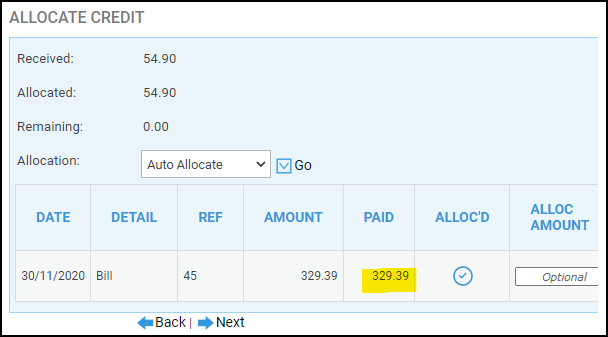

Click Next. Ensure you allocate this posting against the entry being written off also, this should bring the transaction to fully allocated.

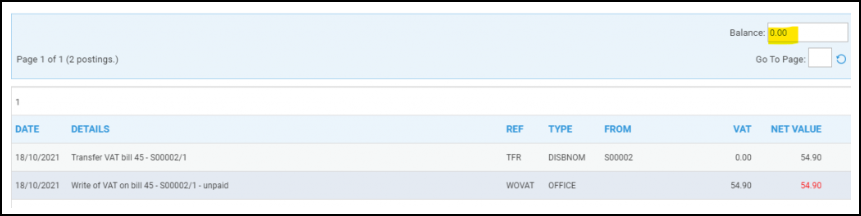

The transactions on the customer’s ledger card are now complete.

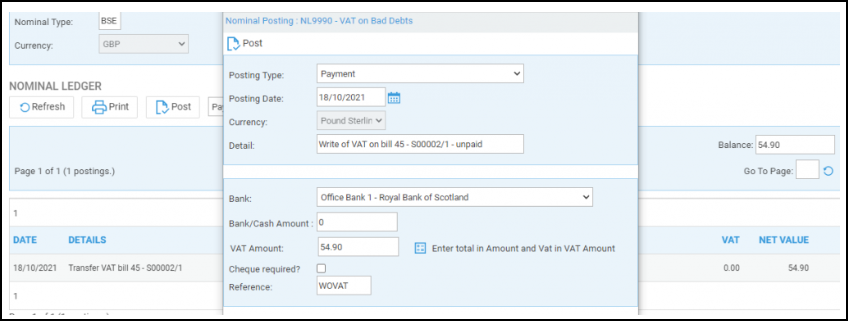

Post the VAT adjustment on the nominal ledger

The last posting (to zero the nominal) is the one which will adjust your VAT input figures, since the transfer to nominal posting beforehand is simply an office amount. Enter the VAT amount to write off in the VAT box, and 0 in the bank/cash amount box.

Click Post.

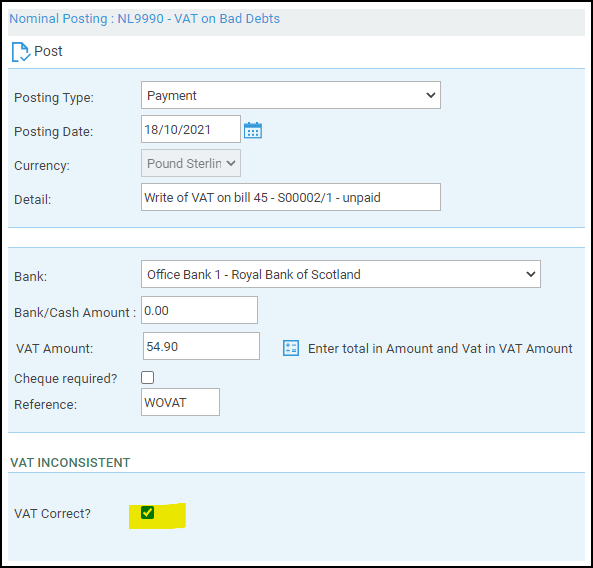

A VAT Inconsistent warning will be displayed at the bottom of the page. If the VAT is correct, select the tick box.

The transaction will clear the balance on your nominal and appear in your VAT return.